April 6, 2026

Market Review: 1Q 2026

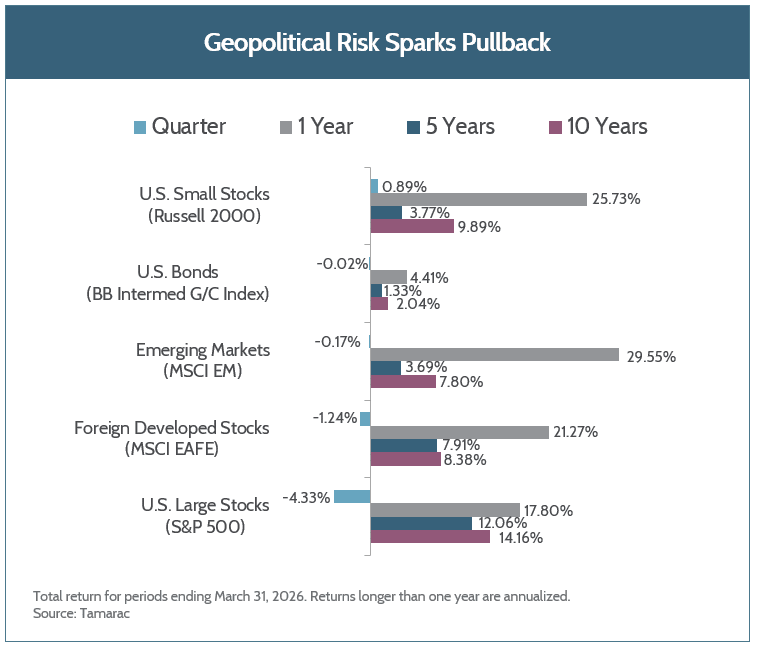

Global markets continued many trends from 2025 into early 2026: foreign stocks outperforming U.S. stocks, the U.S. dollar falling, and interest rates trading in a relatively narrow range. However, as geopolitical risk ramped up in the Middle East, several of these trends reversed. The U.S. dollar rallied a bit, and U.S. stocks began to outperform foreign stocks. Markets have been reasonably calm, with pullbacks within the normal range, especially coming off several years of above-average returns. Oil prices moved significantly higher, and riskier asset classes such as emerging market and US small company stocks sold off the most. One surprising element is that gold also sold off as volatility picked up, which runs counter to the narrative of it being a geopolitical hedge.

There are a few market analogues that rhyme with the current environment. The spike in oil prices due to conflict is reminiscent of the 2022 Russian invasion of Ukraine, and the snarling of supply chains brings back memories of the disruptions caused by COVID, though perhaps on a smaller scale. While both of these events did cause significant disruption in the short run, market forces tend to find solutions over time. The complete fallout from the current disruption remains to be seen.

We believe the U.S. economic backdrop heading into 2026 remains constructive, but rising oil prices, if sustained, are likely to pose an incremental headwind to growth. Higher energy prices flowing through to inflation could inhibit the Fed from lowering interest rates. Should energy prices moderate, prior tailwinds of greater tax savings, business investment, and lower policy rates could once again take hold.

Corporate fundamentals remain positive as large U.S. corporations delivered 13% earnings growth in the first quarter of the year. Coupled with a market pullback, valuations have retreated from elevated levels. In fact, the valuation premium of the technology sector relative to the market is at its lowest level since 2020. With a wide range of external variables at play, quarterly results will take a back seat to what companies say about the path forward.

Even in the face of rising interest rates, bond markets offered insulation from stock market volatility. The main story in lending markets, however, was in private markets. Concerns about AI disruption led to outsized redemption requests from investors. Importantly, company fundamentals, by and large, remain sound, leverage is reasonable, and borrowers continue to make interest and principal payments.

International stocks led U.S. stocks for much of the quarter, then sold off more sharply in the wake of Operation Epic Fury. A rising US dollar was a further headwind to international returns. Global investors appear more concerned about vulnerabilities of foreign companies in an extended conflict that cripples supply chains, particularly those reliant on energy imports or petrochemical products for industrial purposes.

In such environments, we remain on the lookout for risks as well as opportunities with an eye on the long term. Please don’t hesitate to reach out to your Fulcrum wealth manager if you have any questions or concerns.

Unless otherwise noted, data presented in this report is from recognized financial and statistical reporting services or similar sources including but not limited to Reuters, Bloomberg, the Bureau of Labor Statistics, or the Federal Reserve. While the information above is obtained from reliable sources, we do not guarantee its accuracy. This report is limited to the dissemination of general information pertaining to Fulcrum Capital, LLC, including information about our advisory services, investment philosophy, and general economic and market conditions. This communication contains information that is not suitable for everyone and should not be construed as personalized investment advice. Past results are not an indication of future performance. This report is not intended to be either an expressed or implied guarantee of actual performance, and there is no guarantee that the views and opinions expressed above will come to pass. It is not intended to supply tax or legal advice, and there is no solicitation to buy or sell securities or engage in a particular investment strategy. Individual client needs, allocations, and investment strategies differ based on a variety of factors. Any reference to a market index is included for illustrative purposes only, as it is not possible to directly invest in an index. Indices are unmanaged, hypothetical vehicles that serve as market indicators. Index performance does not include the deduction of fees or transaction costs which otherwise reduce the performance of an actual portfolio. This information is subject to change without notice. Fulcrum Capital, LLC is an SEC registered investment adviser with its principal place of business in the state of Washington. For additional information about Fulcrum Capital please request our disclosure brochure using the contact information below.