July 2, 2026

Market Review: 2Q 2026

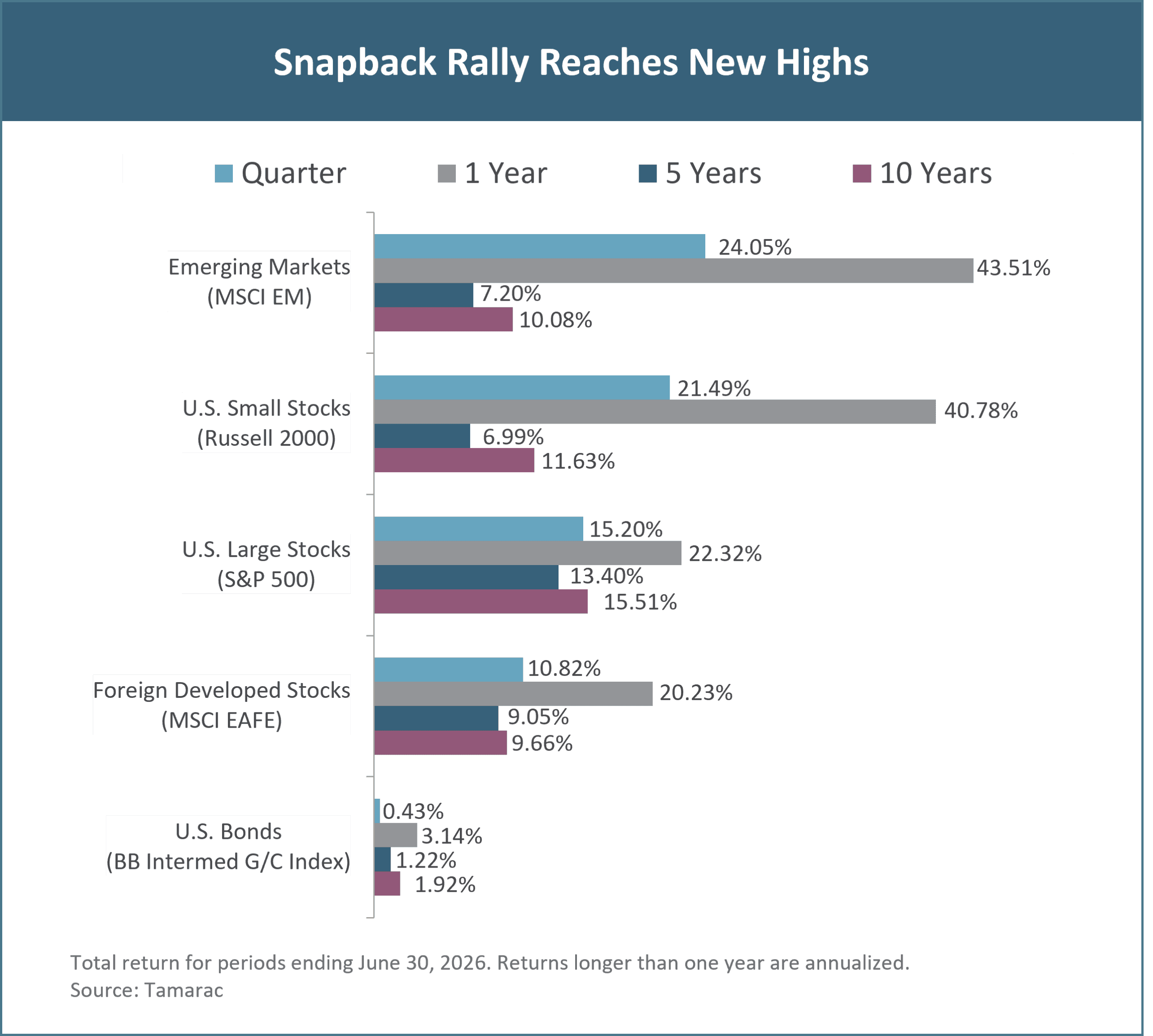

Financial markets staged a dramatic rally to begin the second quarter. Riskier areas of the global stock market, such as emerging markets stocks and U.S. small company stocks, led the way. Bonds also eked out a positive return as fears of renewed inflation from higher energy and input costs subsided. While no clear resolution to the situation in the Strait of Hormuz existed at the time the rally started – and considerable uncertainty remains – market optimism has been somewhat vindicated as activity in the strait has picked up. Several factors kept oil in check as the conflict wore on, but the primary one was a reduction in imports by China. It is difficult to say what the outcome would have been otherwise, but it is hard to imagine it would have been good for the global economy.

Despite temporarily elevated energy prices and broadly firming inflation, the economic picture in the U.S. remains positive. The labor market as a whole is on sound footing, and measures of economic activity are in expansion, particularly in manufacturing. These conditions, along with a new Federal Reserve Chairman, have led to a spirited debate about the trajectory of short-term interest rates dictated by the Federal Reserve. A strong labor market and sticky inflation would seem to support the case for raising interest rates.

Against this backdrop, U.S. corporate fundamentals remain strong. First quarter earnings growth handily surpassed analyst estimates driven by a combination of rising sales and expanding margins. Earnings beats were broad based, with all sectors delivering results above expectations. This strong performance led to upward revisions in earnings estimates, supporting the market’s move higher. Investor optimism has permeated into more risky areas of the market, with unprofitable small company stocks outperforming their profitable peers. Exceptional earnings growth and the outperformance of unprofitable companies are market characteristics typically seen at the earlier stages of an economic cycle. It is difficult to argue that we are currently in the early stages of a cycle, which makes this sort of activity noteworthy.

Emerging market stocks were another area of notable strength during the quarter and provide a good example of how the AI (artificial intelligence) trade has become a global phenomenon. Some of the world’s largest memory-chip manufacturers are located in South Korea, and their stocks have been a significant driver of emerging market index returns. Growing demand for memory, coupled with limited supply, has led to rapidly rising memory-chip prices, and consequently, expanding profit margins.

The strength of AI and AI-related themes has led to many divergences across markets, and we remain on the lookout for both risks and opportunities. Please reach out to your Fulcrum wealth manager if you have any questions or concerns.tomor

Unless otherwise noted, data presented in this report is from recognized financial and statistical reporting services or similar sources including but not limited to Reuters, Bloomberg, the Bureau of Labor Statistics, or the Federal Reserve. While the information above is obtained from reliable sources, we do not guarantee its accuracy. This report is limited to the dissemination of general information pertaining to Fulcrum Capital, LLC, including information about our advisory services, investment philosophy, and general economic and market conditions. This communication contains information that is not suitable for everyone and should not be construed as personalized investment advice. Past results are not an indication of future performance. This report is not intended to be either an expressed or implied guarantee of actual performance, and there is no guarantee that the views and opinions expressed above will come to pass. It is not intended to supply tax or legal advice, and there is no solicitation to buy or sell securities or engage in a particular investment strategy. Individual client needs, allocations, and investment strategies differ based on a variety of factors. Any reference to a market index is included for illustrative purposes only, as it is not possible to directly invest in an index. Indices are unmanaged, hypothetical vehicles that serve as market indicators. Index performance does not include the deduction of fees or transaction costs which otherwise reduce the performance of an actual portfolio. This information is subject to change without notice. Fulcrum Capital, LLC is an SEC registered investment adviser with its principal place of business in the state of Washington. For additional information about Fulcrum Capital please request our disclosure brochure using the contact information below.