January 29, 2025

2026 Market Outlook: Tempered Expectations, Continued Opportunities

2025 was a tumultuous year, but returns across financial markets were surprisingly strong. As we enter 2026, performance expectations across stock and bond markets are more balanced.

The Economy: Broadly Supportive

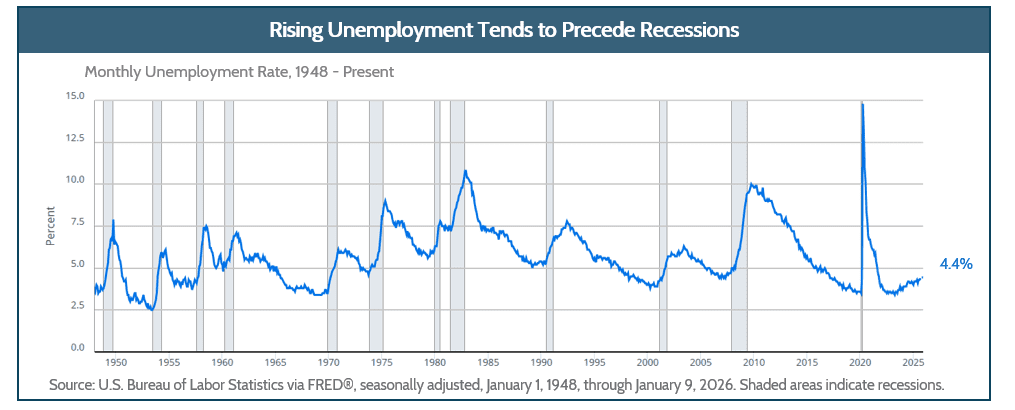

The U.S. economy appears to be entering 2026 on a fairly strong footing. Headwinds from tariffs are fading while tailwinds from legislation are taking hold, and interest rates are poised to decline further. Setting aside a more dynamic geopolitical backdrop, there are two primary risks, which curiously are on opposite sides of the spectrum. One is that an already robust economy receives an extra boost from government spending, which could cause it to overheat and push inflation higher. The other is the trend of rising unemployment and weak job growth. As the chart below shows, once unemployment starts to move higher, it eventually accelerates and results in an economic slowdown or recession. While this has historically been the case, the post-COVID environment has been anything but typical. If the current economic momentum continues into 2026, it’s possible the job market will improve. All things considered, macroeconomic trends appear to be broadly supportive of risk assets.

The Stock Market: Tempered Optimism

Over the long run, there are four underlying drivers of stock returns:

Expected Return = Change in P/E Multiple + Earnings Growth + Dividends + Currency Effect

Changes in Multiples

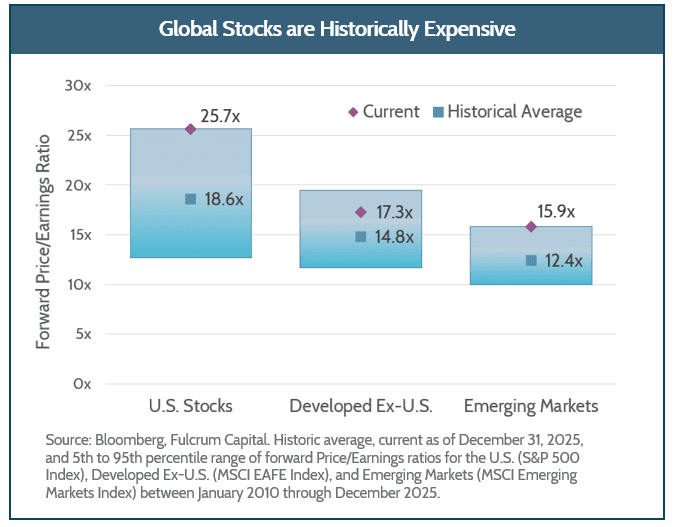

Let’s start by looking at the multiple, or the price paid per dollar of earnings (P/E). Across major global markets, multiples ended 2025 at the higher end of the range for the prior 10 years (chart below). This makes it more difficult to rely on multiple expansions to drive returns in 2026. It’s possible that compression of multiples will be part of the 2026 story. Even international stock markets look somewhat expensive, which is a relatively new development. While they may be cheaper than U.S. stocks, they are expensive relative to their own history. The argument for higher international stock allocations can no longer rely solely on valuation. For both US and international stocks, elevated valuations set a high bar for corporate execution and leave less room for negative surprises to be absorbed without impacting stock price.

Earnings and Dividend Growth

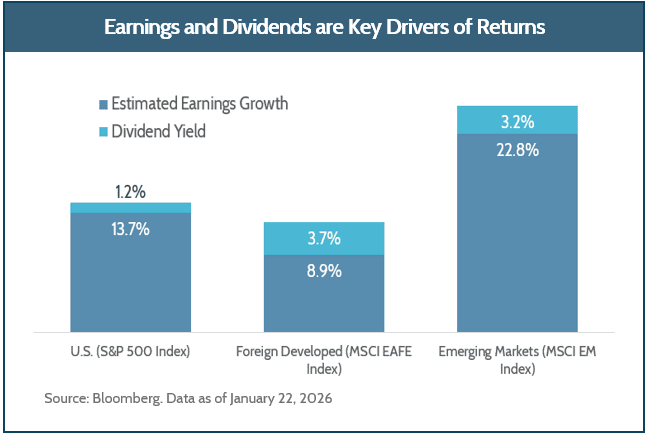

This means returns will be driven primarily by dividends, earnings, and in the case of international stocks, currency movements. Earnings and, to a lesser extent, dividends were the primary drivers of return for the S&P 500 in 2025, providing good example of how this can lead to positive outcomes. Looking ahead to 2026, analyst expectations for earnings growth for U.S. stocks are 13.7%, though dividend expectations remain relatively muted. (See chart below.)

Analysts are typically overly optimistic at the start of the year, so we should take these earnings expectations with a grain of salt. But even if we reduce those forecasts and factor in lower valuations, there’s still room for reasonable returns, though certainly less than in the last few years. If rising valuations turn out to be what drives returns in 2026, that will look a lot more like a bubble.

One key theme driving U.S. stock markets in recent years is artificial intelligence (AI) and it’s likely to be a driver once again in 2026. A primary question on the minds of investors is the return on investment from AI-related capital expenditures. Missed expectations on this front could be a catalyst for reduced earnings growth expectations as well as some multiple compression. Such an outcome would favor other areas of the stock market that were neglected in favor of the AI theme.

Looking abroad, earnings growth is expected to be strongest in emerging markets. This could potentially result in solid returns, even in the face of multiple compressions, though a repeat of 2025’s 30%+ returns seems unlikely. Meanwhile, earnings growth expectations are lower in foreign developed markets, and investors rely more heavily on dividends for returns on those stocks.

Currency

Turning to the fourth element in the return equation, currency provided a healthy tailwind for foreign stock returns in 2025. The drop in the U.S. Dollar accounted for nearly one-third of the performance of foreign developed stocks, although the benefit was less pronounced in emerging markets. While predicting currency movements is very challenging, the U.S. dollar has tended to move in multi-year cycles. The recent decline could indicate a downward trend over the coming years, which would benefit foreign stocks.

All in, after a strong year across global stock markets in 2025, it seems prudent to temper expectations in 2026. However, that does not mean we won’t have another positive year in 2026.

The Bond Market: A “Coupon” Year

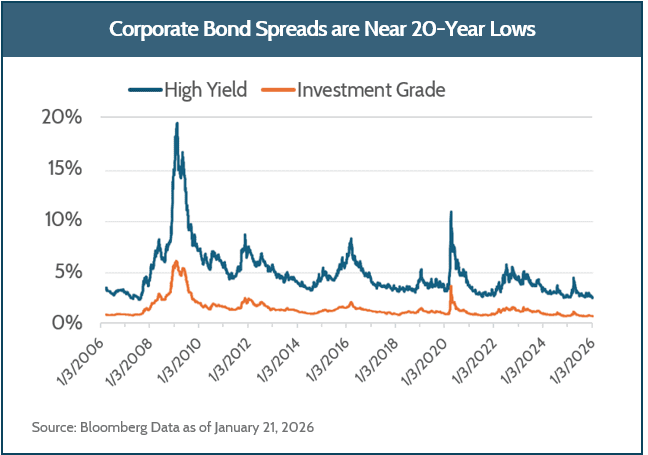

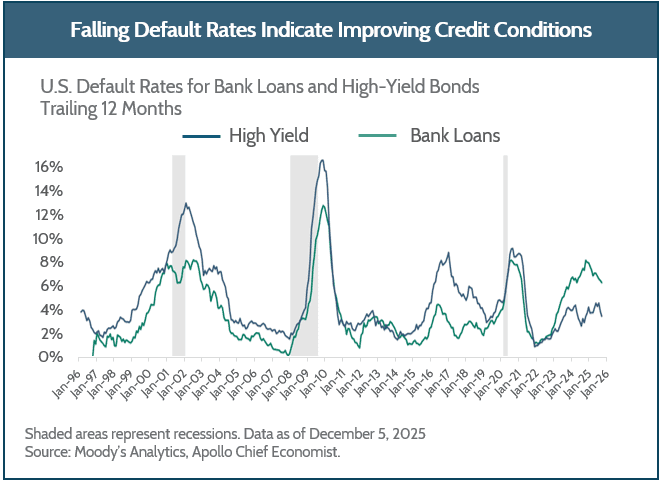

In bond markets, we see similar evidence of investor optimism after one of the best years for bonds of the past decade. One way to quantify the optimism is to look at the difference – or spread – between borrowing rates for corporations and borrowing rates for the U.S. government. In both investment-grade and below-investment-grade (high yield) bonds, spreads are at or near the lowest they have been in several decades. This indicates investors earn less additional yield for taking on risk than in the past. With corporations broadly in good health and default rates on the decline, low spreads have the potential to persist.

After a solid year in bond markets, it makes sense to temper expectations here as well. Unless we see new problems or distress in credit markets, it is potentially a “coupon” type of year, where the starting yield is a reasonable measure of expected return. Key risks to the bond market are a strong economy that keeps the Fed from lowering rates and rising inflation.

This environment may also demonstrate the benefit of seeking yield outside of traditional public bond markets. Private debt markets continued to be a source of higher yields this year as banks pull away from middle-market and specialty lending. As with other forms of debt, direct lending spreads compressed in 2025 but remain attractive with yields near double digits. The year ahead may require more patience than recent years, but long-term investors may still be rewarded. It’s important to remember that long-term investment success comes from realistic expectations, thoughtful diversification, and the discipline to stay invested through a year of transition.

Unless otherwise noted, data presented in this report is from recognized financial and statistical reporting services or similar sources including but not limited to Reuters, Bloomberg, the Bureau of Labor Statistics, or the Federal Reserve. While the information above is obtained from reliable sources, we do not guarantee its accuracy. This report is limited to the dissemination of general information pertaining to Fulcrum Capital, LLC, including information about our advisory services, investment philosophy, and general economic and market conditions. This communication contains information that is not suitable for everyone and should not be construed as personalized investment advice. Past results are not an indication of future performance. This report is not intended to be either an expressed or implied guarantee of actual performance, and there is no guarantee that the views and opinions expressed above will come to pass. It is not intended to supply tax or legal advice, and there is no solicitation to buy or sell securities or engage in a particular investment strategy. Individual client needs, allocations, and investment strategies differ based on a variety of factors. Any reference to a market index is included for illustrative purposes only, as it is not possible to directly invest in an index. Indices are unmanaged, hypothetical vehicles that serve as market indicators. Index performance does not include the deduction of fees or transaction costs which otherwise reduce performance of an actual portfolio. This information is subject to change without notice. Fulcrum Capital, LLC is an SEC registered investment adviser with its principal place of business in the state of Washington. For additional information about Fulcrum Capital please request our disclosure brochure using the contact information bel